Facebook

Facebook

Twitter

Twitter

Pinterest

Pinterest

Copy Link

Copy Link

It’s that time of year when Windermere’s Chief Economist, Matthew Gardner, dusts off his crystal ball and peers into the future to give us his predictions for the 2020 economy and housing market.

First posted on windermere-bellevue.com

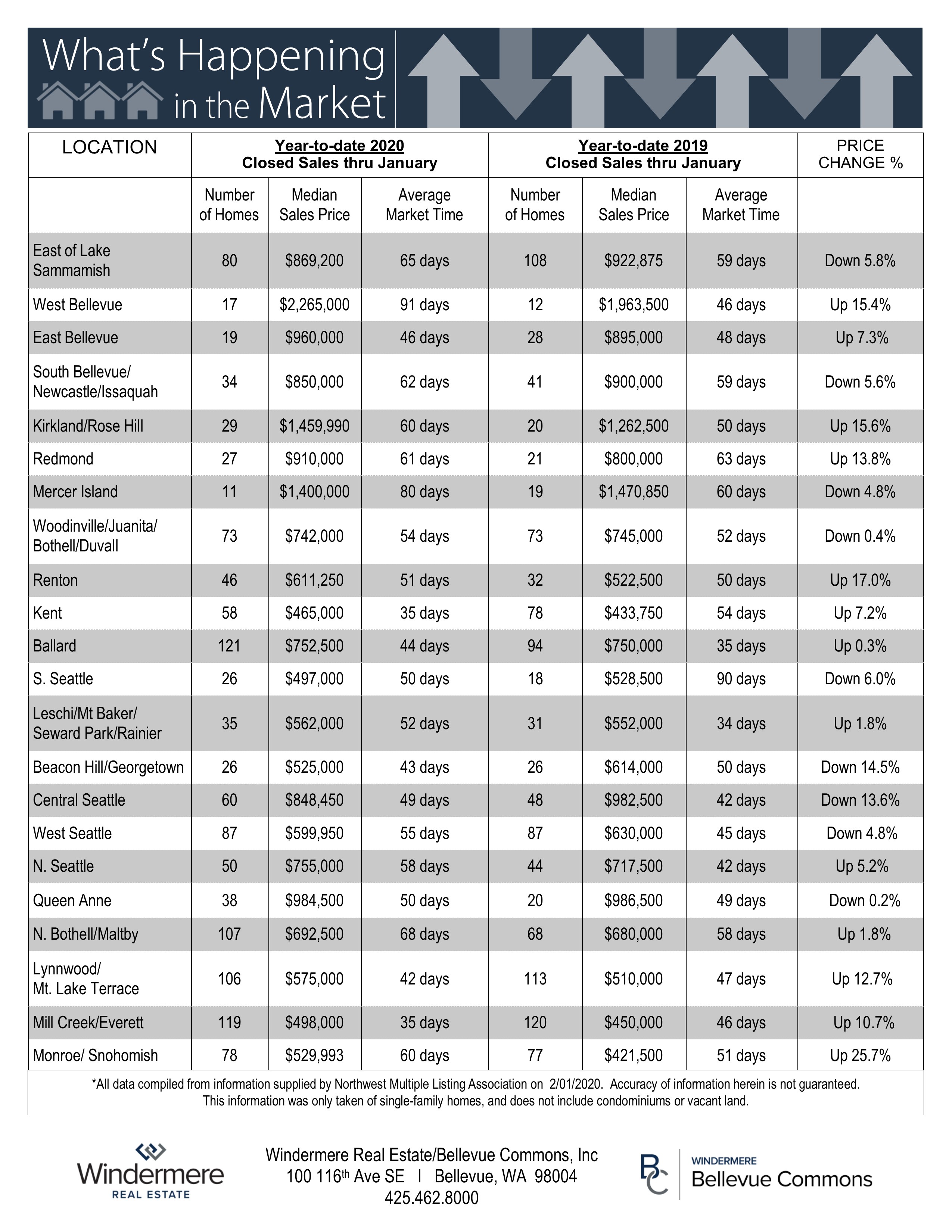

As expected, the market has drastically picked up due to extremely low inventory and heighted Buyer activity that had been holding off purchasing during the holidays. Since these stats are not a rolling 12 month average they are going to appear skewed due to the small sample size, but they do show year over year with many areas growing significantly from January 2019. Pretty much every market has been on fire with Multiple offers on just about everything available for sale. The Days on Market (DOM) have dramatically gone up, but that is primarily due to homes selling that had been on the market for a while that Sold over the holidays. We expect to see the DOM fall significantly over the next couple months as most new listings are now selling in under 14 days & in many cases less than a week. (Pro Tip- Buyers be prepared to put your best foot forward & Sellers to make sure their home is parade ready to get the highest dollar!)

The increased amount of viewership of listings on Realtor.com in January 2019 shows that Buyer interest is absolutely heightened in January around the Puget Sound more than any place due to the limited inventory and the shear amount new jobs being created in our marketplace. This trend shows there is no better time to list a property than now, when the Buyers are actively looking.

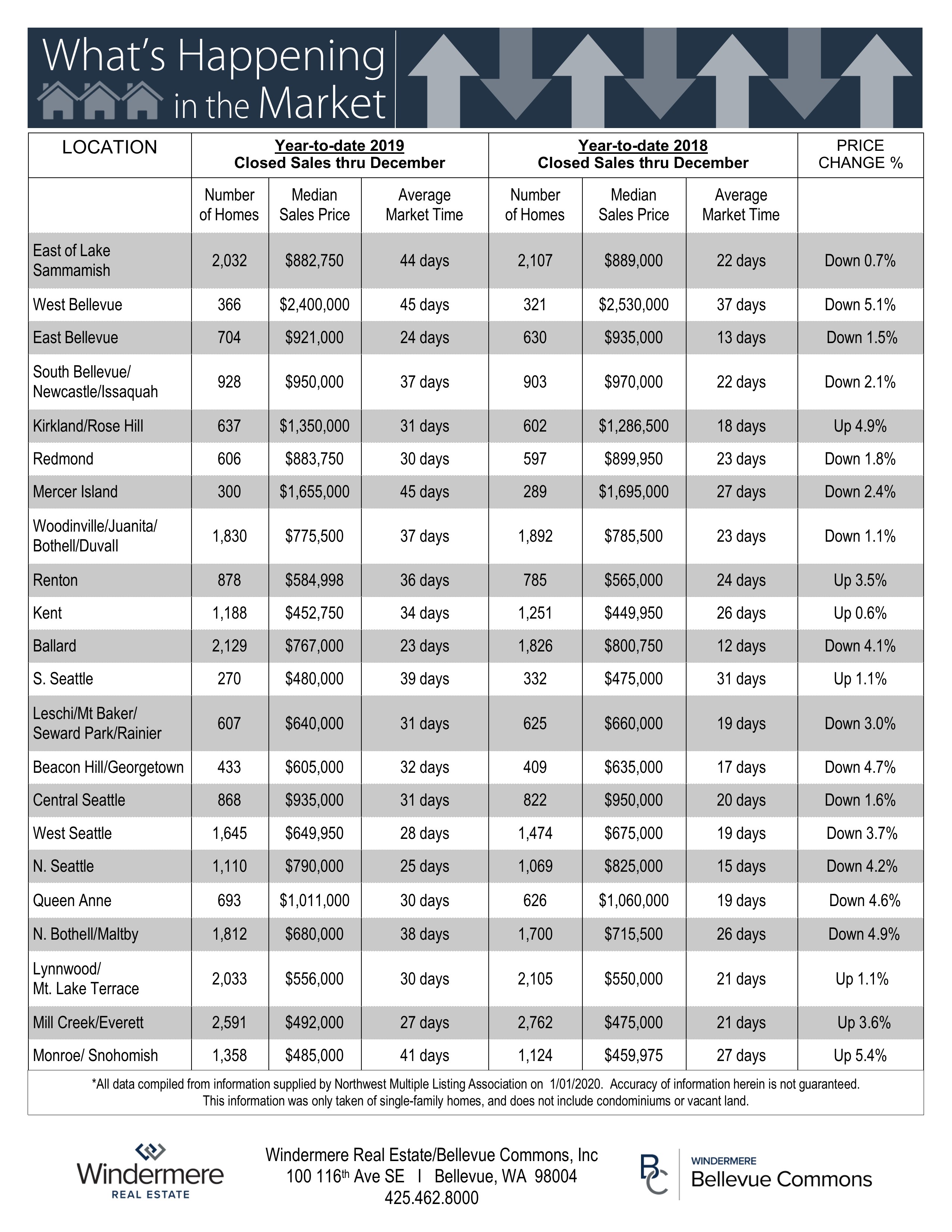

“December 2019 stats show that we are creeping in on the highs we saw in 2018 in most areas and in several other areas prices have already surpassed the previous year. Inventory is now below 1 month which means if there weren’t anymore listings coming on the market there would be nothing to buy in 4 weeks. December 2019 Pendings were up 11% over last December and it appears that momentum is going to carry into a very busy January 2020. Sellers are in an great position right now and those listings that are positioned correctly (Price/Condition) are once again looking at multiple offers.”

– Inventory across the NWMLS at the end of December was down 31% from last December.

– Inventory in King County was down 38.8% (Condo and Residential Combined) while Single family was down 41.1%. Currently sitting at 0.9 Months across King, Kitsap, Snohomish and Pierce counties.

– Median Prices across the Puget Sound (4 Counties- King, Kitsap, Snohomish and Pierce) were up 10% while King county rose 3%. This is primarily due to much more New Construction up North and down South.

– Closed sales across the NWMLS in December were up 11% from last December.

– King County is starting to see Multi-Million-dollar sales being purchased with cash at a much higher rate than the previous couple years.

– Rental Properties are very tight as anything New is being reserved prior to being finished.

– Opportunities for Buyers prior to the Spring market are starting to dwindle and Sellers waiting for the Spring market may see an inordinate amount of competition.

– January 2020 may turn out to be the start of the New Spring Market!

It was a great year! We enjoyed celebrating the upcoming holidays with our clients and partners! It means a lot to us to be a part of such an important journey in your life. Thank you for allowing us to serve your Real Estate needs.

Thank you for coming and Happy Holidays!

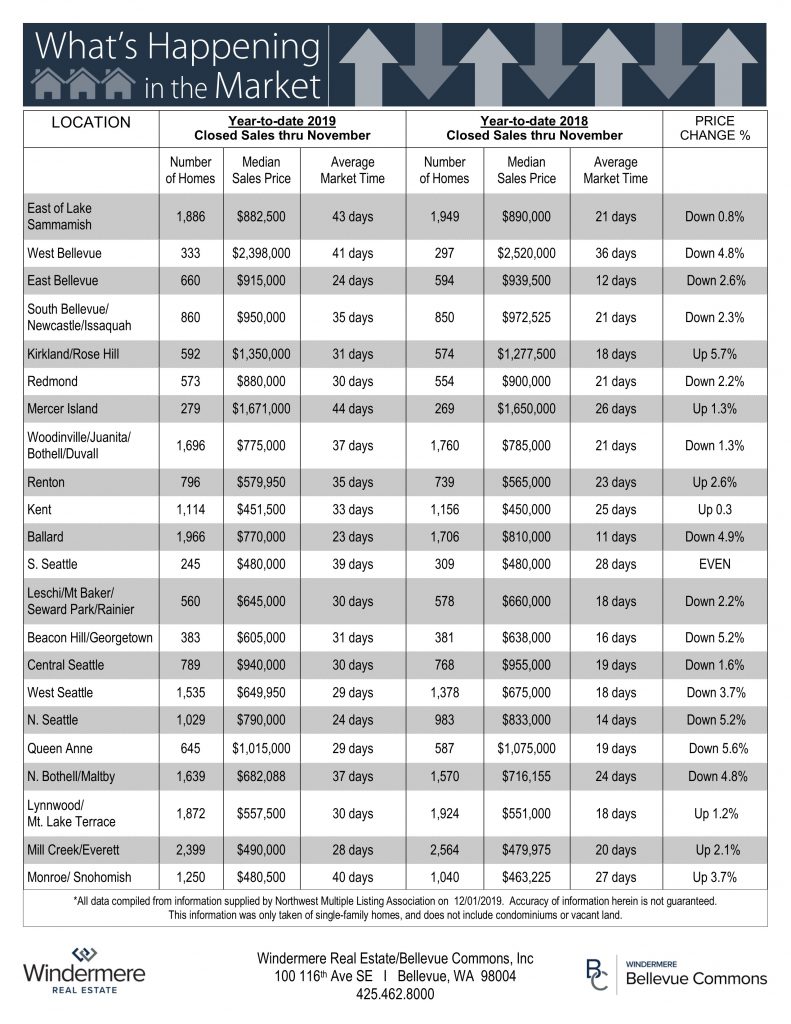

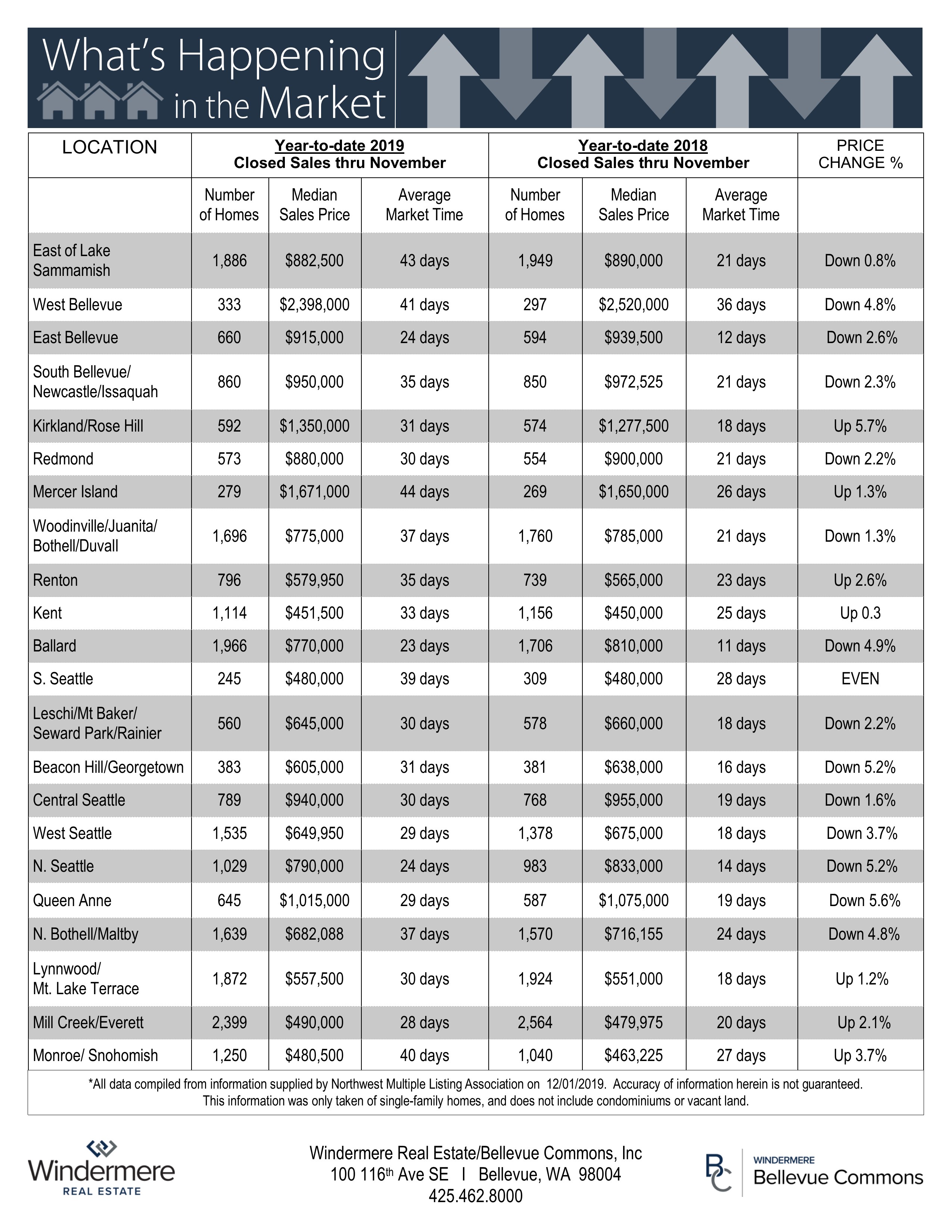

Buying/Borrowing Power is now up 12% due to extremely low interest rates (Roughly 3.70%) compared to this time last year while prices are continuing to climb and have reached 2018 prices in most areas. November pendings were up 20% over last November effectively reducing available properties towards all-time lows where we are currently standing at 1.2 months of inventory. There doesn’t seem to be any relief in the near future with a flood of new tech jobs entering the marketplace, but Buyers are still being very selective about purchasing properties that are in turn key condition.

First posted at windermere-bellevue.com

A steady influx of buyers continued to strain already tight inventory throughout the area in October. Home sales were up, as were prices in much of the region. With our thriving economy and highly desirable quality of life drawing ever more people here, the supply of homes isn’t close to meeting demand. Homeowners thinking about putting their property on the market can expect strong buyer interest.

As the Eastside continues to rack up “best places” awards, it’s no surprise that the area is booming. Development is on the rise, fueled primarily by the tech sector. The appeal of the Eastside has kept home prices here the highest of any segment of King County. The median single-family home price in October was stable as compared to the same time last year, rising 1% to $900,000.

King County’s 1.74 months of available inventory is far below the national average of four months. Despite the slim selection, demand in October was strong. The number of closed sales was up 5% and the number of pending sales (offers accepted but not yet closed) was up 11%. The median price of a single-family home was down 2% over a year ago to $660,000. However, some areas around the more reasonably-priced south end of the county saw double-digit price increases.

Seattle home prices took their largest year-over-year jump in 12 months. The median price of a single-family home sold in October was up 3% from a year ago to $775,000, a $25,000 increase from September of this year. Seattle was recently named the third fastest-growing city in America. Real estate investment is surging. A growing population and booming economy continue to keep demand for housing –and home prices—strong.

Both the number of home sales and home prices were on the rise in Snohomish County in October. Overall homes sales increased 7%, and the median price of a single-family home rose 5% over a year ago to $495,000. Supply remains very low, with just six weeks of available inventory.

VIEW FULL SNOHOMISH COUNTY REPORT

This post originally appeared on GetTheWReport.com

The following analysis of the Western Washington real estate market is provided by Windermere Real Estate Chief Economist, Matthew Gardner. We hope that this information may assist you with making better-informed real estate decisions. For further information about the housing market in your area, please don’t hesitate to contact your Windermere agent.

ECONOMIC OVERVIEW

Washington State employment has softened slightly to an annual growth rate of 2%, which is still a respectable number compared to other West Coast states and the country as a whole. In all, I expect that Washington will continue to add jobs at a reasonable rate though it is clear that businesses are starting to feel the effects of the trade war with China and this is impacting hiring practices. The state unemployment rate was 4.6%, marginally higher than the 4.4% level of a year ago. My most recent economic forecast suggests that statewide job growth in 2019 will rise by 2.2%, with a total of 88,400 new jobs created.

HOME SALES

HOME PRICES

DAYS ON MARKET

CONCLUSIONS

This speedometer reflects the state of the region’s real estate market using housing inventory, price gains, home sales, interest rates, and larger economic factors. I am leaving the needle in the same position as the first and second quarters, as demand appears to still be strong.

The market continues to benefit from low mortgage rates. The average 30-year fixed rates is currently around 3.6% and is unlikely to rise significantly anytime soon. Even as borrowing costs remain very competitive, it’s clear buyers are not necessarily jumping at any home that comes on the market. Although it’s still a sellers’ market, buyers have become increasingly price-conscious which is reflected in slowing home price growth.

ABOUT MATTHEW GARDNER

As Chief Economist for Windermere Real Estate, Matthew Gardner is responsible for analyzing and interpreting economic data and its impact on the real estate market on both a local and national level. Matthew has over 30 years of professional experience both in the U.S. and U.K.

As Chief Economist for Windermere Real Estate, Matthew Gardner is responsible for analyzing and interpreting economic data and its impact on the real estate market on both a local and national level. Matthew has over 30 years of professional experience both in the U.S. and U.K.

In addition to his day-to-day responsibilities, Matthew sits on the Washington State Governors Council of Economic Advisors; chairs the Board of Trustees at the Washington Center for Real Estate Research at the University of Washington; and is an Advisory Board Member at the Runstad Center for Real Estate Studies at the University of Washington where he also lectures in real estate economics.

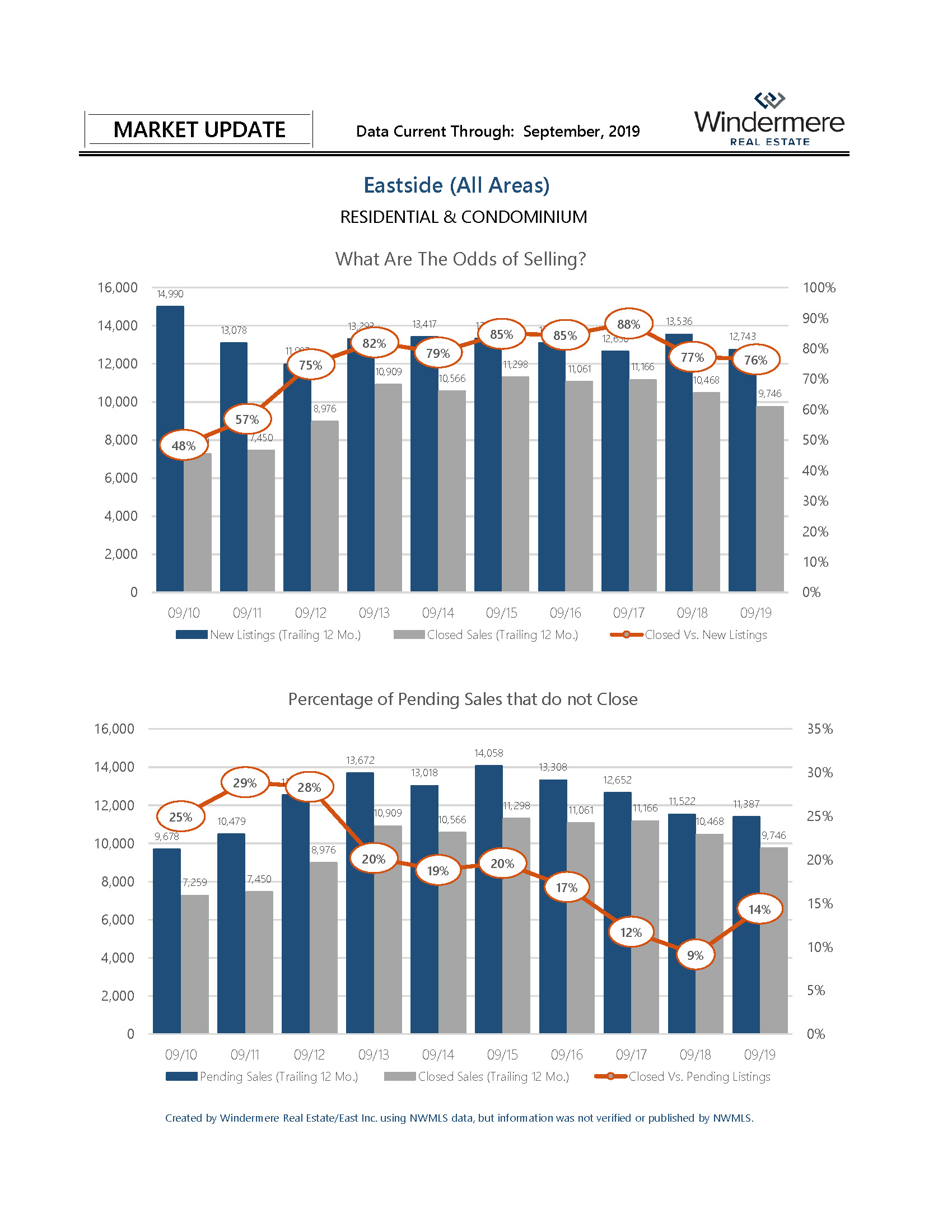

• Sales are good (pending sales up 9% for September vs last year 931 vs 857). Inventory is down 21% from a year ago (1,713 vs 2,161).

• Sales up and inventory down is good for sellers, but it does not feel too good. Prices are flat. Only 18% of September closings were for over list price compared to 60% in the hot hot markets (spring of 2017 & 2018). Finally, about half (46.8%) of properties that sold, sold with less than 15 days of Days on Market. List price must be close to value to sell.

• Interest Rates, Interest Rates, Interest Rates… 3.61% vs 4.63% from a year ago (page 5).

A one percent change in interest rate is a 10% change in purchase price.

• Competing for a listing? (share from page 2)

1. What are the odds of selling 3 in 4 (75% for trailing 12 months), 1 in 4 are not selling.

2. Percentage of Pending Sales that don’t close is 1 in 8 (14% for trailing 12 months)

Who you hire matters!

A decrease in inventory coupled with an increase in sales activity led to fewer options for home shoppers in August. There is some good news for would-be buyers as mortgage rates have dropped to their lowest level in three years. Demand remains high but there simply aren’t enough homes on the market. Brokers are hoping to see the traditional seasonal influx of new inventory as we move forward.

The median price of a single-family home on the Eastside was $935,000 in August, unchanged from a year ago and up slightly from $925,000 in July. New commercial and residential construction projects are in the works. Strong demand for downtown condos has prompted plans for yet another high-rise tower to break ground next year.

Home prices in King County were flat in August. The median price of a single-family home was $670,000, virtually unchanged from a year ago, and down just one percent from July. Southeast King County, which has some of the most reasonable housing values in the area, saw prices increase 9% over last year. Inventory remains very low. Year-over-year statistics show the volume of new listings dropped 18.5% in King County.

Homes sales were up 12% in Seattle for August, putting additional pressure on already slim inventory. There is just over six weeks of available supply. There are signs that prices here are stabilizing as the median home price of $760,000 was unchanged from a year ago and up less than one percent from July. With its booming economy, demand here is expected to stay strong.

Buyers looking for more affordable options outside of King County pushed pending sales, mutually accepted offers, up nearly 16% over a year ago. Home prices have softened slightly. The median price of a single-family home in August was $490,000, down slightly from the median of $492,225 the same time last year.

VIEW FULL SNOHOMISH COUNTY REPORT

This post originally appeared on GetTheWReport.com